Welcome

- Home

- About Us

- Book a Valuation

- FREE Instant Valuation

- Meet The Team

- Independent Customer Reviews

- GBP Estates Blog

- Guild Membership

- Guild Market News

At GBP Estates we believe in keeping you informed about what is going on in the property market.

23 April 2024

As we are now nicely into 2024, it's certain the Romford housing market over the last 18 months has been a little more restrained than 2020, 2021 and early 2022, and I believe that...

17 April 2024

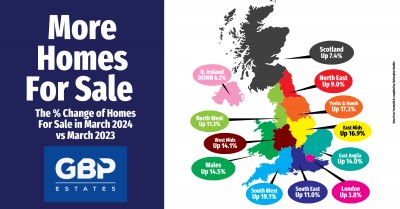

The UK housing market is bustling with activity as shown in our latest March 2024 property market data, revealing some changes from just a year ago in March 2023. There's a...

16 April 2024

Understanding the nuances of property sales is essential for both homeowners and investors in the dynamic Romford property market. A few weeks ago, I stated that of the...

11 April 2024

In the articles on the Romford property market, we like to provide an insight into the real story of what is happening in our Romford (and national) property market and address the...

4 April 2024

Many Romford people I talk to in their late 30s to late 40s are relying on the inheritance from their Baby boomer generation parents to help them in their home buying and...

26 March 2024

Whether you are a Romford landlord looking to liquidate your buy-to-let investment or a Romford homeowner looking to sell your home, finding a buyer and then getting the legal work done can take a...