Welcome

- Home

- About Us

- Book a Valuation

- FREE Instant Valuation

- Meet The Team

- Independent Customer Reviews

- GBP Estates Blog

- Guild Membership

- Guild Market News

At GBP Estates we believe in keeping you informed about what is going on in the property market.

3 August 2026

When people talk about the property market in Romford, the conversation normally centres on house prices. Yet price is only part of the story. The size of a home matters too. A...

27 July 2026

Every few weeks, another headline appears warning that house prices are about to crash. The reason changes each time. One month it is mortgage rates. The next it is inflation. More recently,...

17 July 2026

As an agent in the Romford property market, I believe it is important to offer local homeowners a balanced and realistic view of both the Romford and national property markets. Far too...

11 July 2026

The Romford property market can often feel far more active than it really is. Every week, new for sale boards appear outside people’s homes on your street. You tell yourself, ‘They...

2 July 2026

For some homebuyers, the kitchen is the deal maker. For others, it is the number of bedrooms, the school catchment or the distance to the railway station. Yet for a sizeable group of buyers, the...

24 June 2026

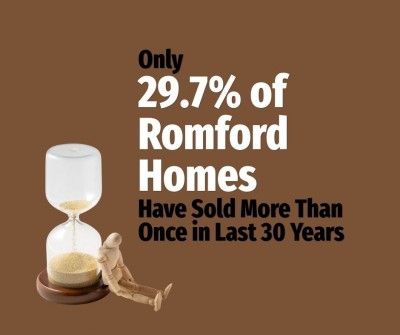

There is a quiet unspoken problem sitting inside the Romford property market. In the last two years, only 56.68% of the homes that came on the market have ended up selling....